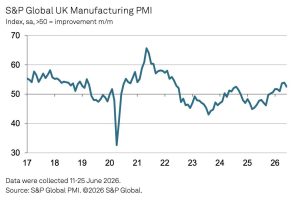

Output growth accelerates as the manufacturing PMI posts at 52.5 in June

The upturn in UK manufacturing showed signs of losing momentum at the end of the second quarter. Although output growth accelerated as companies continued to benefit from clients’ strategic stockpiling, a softer uplift in incoming new orders suggested the impetus provided by this was already starting to fade.

The seasonally adjusted S&P Global UK Manufacturing Purchasing Managers’ Index™ (PMI®) posted 52.5 in June, down from May’s four-year high of 53.9 and the earlier flash estimate of 53.1. The PMI has signalled expansion in each of the past eight months.

Four of the five PMI sub-components were at levels consistent with improved operating conditions. Output, new orders and employment all expanded and suppliers’ delivery times lengthened. The positive signal suggested by the latter (vendor delivery times) may be slightly misleading, given it was mainly reflective of stretched supply chains as opposed to a substantive increase in demand for inputs. Stocks of purchases fell following a solid rise in the prior survey month.

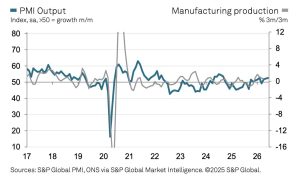

Manufacturing production expanded for the third month running in June, with the rate of growth improving to a 21-month high. Increased output was often linked to higher new work intakes, better market confidence and promotional activities. The consumer and intermediate goods industries both saw growth of production volumes, in contrast to a downturn in the investment goods category.

New work inflows improved for the seventh consecutive month in June, with reports of mild upticks in demand from both domestic and overseas clients. The rate of expansion eased to its weakest since December 2025.

June saw new export business increase for the sixth month in a row, albeit only mildly and to the weakest extent during that sequence. Expansions in the consumer and investment goods sectors were partly offset by a decrease at intermediate goods producers. Growth of foreign demand was linked to improved new work intakes from mainland China, the EU and the US. Several firms noted that growth opportunities in the Middle East had stalled as a result of war in the region.

The outlook for the manufacturing sector remained tepid at the end of the second quarter. Although a plurality of survey respondents (48%) forecast output to rise over the coming year, this was slightly below the combined level of those expecting either stagnation (44%) or contraction (9%).

Manufacturers expecting an upturn in output volumes over the next 12 months mainly linked this to new market opportunities, product launches, use of new technologies (including AI and data centres) and market stabilisation. However, several also noted ongoing concerns about government policy and geopolitical tensions, with some also mentioning they were concentrating more on consolidation during the coming year than towards growth.

Although manufacturing employment rose for the third successive month, the rate of job creation remained only modest. A number of firms mentioned that the potential hiring benefits of rising output and new order intakes were being offset by the need to trim (or freeze) headcounts in some areas due to ongoing market uncertainty and rising input costs.

Average input prices rose markedly in June. Although the rate of increase remained elevated, it was the weakest since March. Supply chain disruptions, material shortages and geopolitical tensions all exerted upward pressure on purchasing costs. Subsequently, average output charges were raised for the seventh month running, with the rate of increase remaining relatively close to May’s near four-year high.

Vendor delivery times continued to lengthen to a marked extent in June, as supply chains remained under substantial duress due to global shipping delays, material shortages, port and regulatory issues, tariff disruptions and capacity shortages at vendors.

Rob Dobson, Director at S&P Global Market Intelligence, commented: “The UK manufacturing sector ended the second quarter of the year on a positive note, with output expanding at the fastest pace since September 2024.

“Sustaining the upturn is becoming a bigger concern. Manufacturers are currently benefiting from client strategic stockpiling, as they safeguard against supply chain disruptions and expected price rises. A drop in the rate of growth of new work intakes suggests this boost is already starting to fade.

“Manufacturers’ optimism about the year ahead also remains tepid, with many concerned about geopolitical tensions and uncertain over the future course of government policy.

“There was mixed news on the prices front. Although input cost inflation remained elevated as severely strained supply chains led to raw material shortages and higher vendor charges, the recent drop in energy prices has helped reduce the overall rate of inflation, leading to a similarly welcome slowing in the rate of increase of factory selling prices.”

Abu Ali, partner at FRP Corporate Finance, said: “The sector is still demonstrating resilience, even as activity eases after last month’s strong performance. Demand remains uneven in places, but manufacturers continue to adapt and maintain output despite ongoing pressure on costs and margins.

“Initially, it was hoped that the peace agreement between Iran and the US would ease some pressure on energy markets and global supply chains. However, businesses are unlikely to become complacent, as the agreement now comes under strain. Many will be watching closely to see whether renewed pressure will feed into costs and confidence in the coming months.

“Firms are also awaiting political clarity following Sir Kier Starmer’s resignation. With more than half of manufacturing leaders saying energy costs are the biggest factor shaping strategic decisions, they will be looking for an administration that prioritises energy policy to create the confidence needed to drive growth.”

John Bryant, head of manufacturing at MHA, commented on today’s S&P Manufacturing PMI data: “June’s PMI figures show a manufacturing sector still growing, but with momentum feeling more fragile as the index fell to 52.5. The recent uplift appears to have been temporary, driven in part by customers stockpiling ahead of expected price rises and disruption linked to the conflict in the Middle East. With new order growth now at a six-month low, there are clear signs that this boost is already fading.

“Similarly, employment growth is a positive signal, but it should be treated with caution. Some firms say recent hiring is a short-term response to stronger order books rather than evidence of lasting confidence.

“Manufacturers continue to face significant pressure. Energy costs remain a major challenge, cited as a key operational risk by 33% of firms in our latest Manufacturing report. Supply chains are also under strain. Our report shows supply chain disruption is now the sector’s biggest operational risk, cited by 35% of firms.

“Further pressures are also building. The introduction of US steel tariffs, the forthcoming Carbon Border Adjustment Mechanism and a new Prime Minister all point to more change and less stability. Manufacturers want certainty, but ongoing geopolitical tensions, supply chain disruption and a difficult economic backdrop do not create the conditions businesses need to plan, grow or invest.

“Despite this, manufacturers are not standing still. Our report shows that more than four in five manufacturers expect growth of at least 3% over the next year, while 26% expect growth above 5%. Many are also investing in technology, AI, IT systems and more diverse supply chains to build resilience.

“However, our report points to clear regional disparities, with manufacturers in different parts of the UK facing distinct pressures depending on their local skills base, infrastructure, supply chains and levels of digital adoption. This underlines the need for a more regional approach to industrial policy, with regional mayors playing a stronger role in directing support, funding and skills programmes towards the specific needs and strengths of their local manufacturing economies.

“The sector has clear ambition, but turning short-term growth into sustained recovery will depend on stronger demand, lower cost pressure and a more stable policy environment.”

Mike Thornton, Head of Industrials at RSM UK, said: “UK manufacturers continue to show resilience. Strong demand and front-loaded orders have maintained a strong start to the year, but there are early signs that momentum is softening with new orders and hiring both easing this month. The good news is that confidence in future output remains strong, suggesting any slowdown could be short-lived.

“If the peace accord holds then any inflationary pressure working its way through supply chains since the conflict in Iran started will begin to ease. The reopening of the Strait of Hormuz will support global trade flows, improve the movement of materials and help bring energy costs back down.

“However, the effects of recent disruption are still likely to feed through in the coming months, meaning the current expansion story should be viewed with a degree of caution. While global tensions may be easing, domestic political uncertainty could create fresh challenges for businesses. As a result, the outlook for UK manufacturing in 2026 appears more complex than the headline figures suggest.”

Thomas Pugh, chief economist at RSM UK, said: “The output balance of the PMI climbing to a 21-month high suggests that firms continued to try to front-run potential price increases in June which is continuing to boost activity. That said, this momentum can’t last forever, and the new orders balance dropped to the lowest since December 2025, which could suggest that activity will fall back sharply over the summer.

“In any case, the drop in the input price balance should provide some relief to firms. That said, both the input and output price balances remain elevated, which suggests there is enough inflation in the pipeline already that core goods inflation is still likely to pick up towards the end of the year. Fortunately, the input and output price balances should continue to ease, as seen by the downwards revision between the flash and final PMI, as oil prices are now back at pre-war levels which should mean any pickup in inflation is brief.

“The improved outlook for inflation lowers the risk of the Bank hiking later this year. This, combined with the unwinding of front-running and persistent political uncertainty which will weigh on activity means we continue to expect the Bank of England to remain on hold before resuming cuts in 2027.”

Read other recent UK Manufacturing news: https://uk-manufacturing-online.co.uk/category/news/

{kind=link}